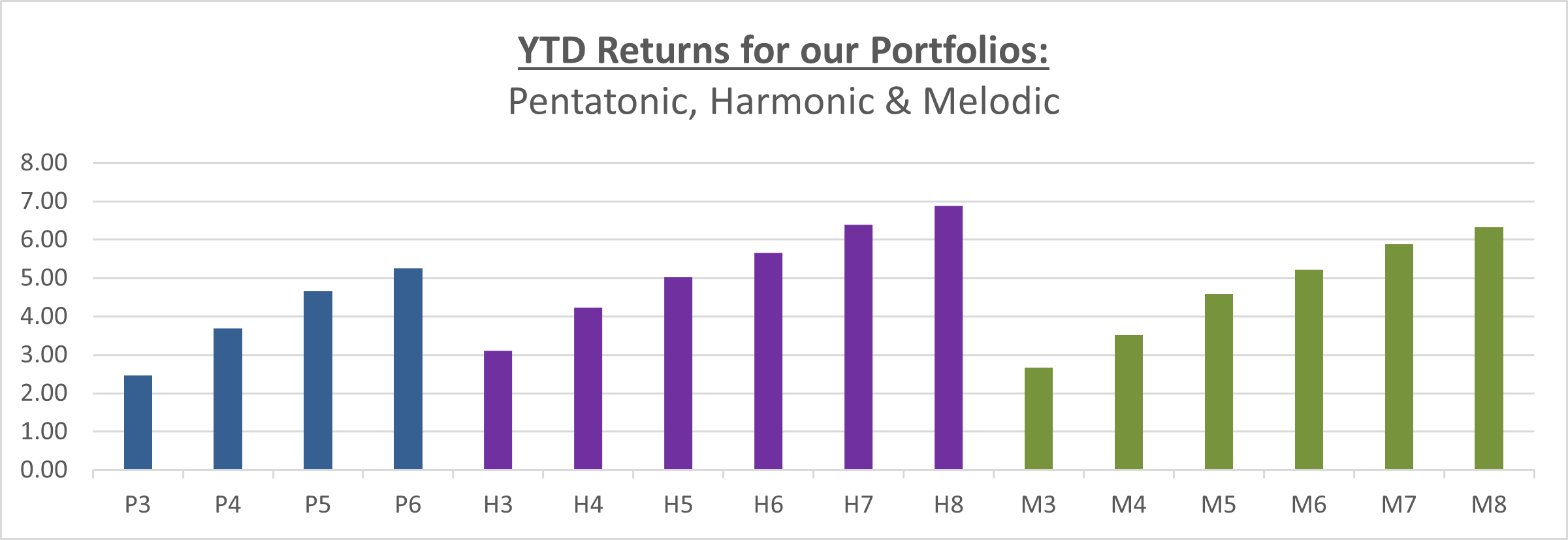

Model Portfolios have all shown a positive return since January 1st as the following table shows. The returns per portfolio are an indication only and are to identify the growth per level of risk within each portfolio range.

(click chart to enlarge)

I have reduced the portfolio return by the maximum ongoing fee a client could pay (except Offshore Bond investors). The figures for the Pentatonic Income Portfolio assume income is reinvested as I am unable to strip out the dividend that has been paid.

Market summary 2nd Quarter 2021

The end of Q2 2021 saw global equities rally as a result of the ever-accelerating covid-19 vaccinations and the world returning to some sort of normality.

Here are some observations of a few areas we invest in.

Europe

With many European countries seeing Covid infections falling, and restrictions being lifted on social and economic activities, Eurozone shares increased.

Some of the sectors which were lagging throughout Q1 ended up being some of the top performing sectors in Q2 as a result of the vaccine roll out. For example, consumer staples and real estate were two of the main winners in Q2 along with the IT sector. Utilities and Energy sectors were the main sectors which saw the lowest movement throughout Q2.

Inflation throughout Europe reduced slightly by the end of Q2, this coupled with the European commission signing off the first of their national recovery plan funding helped the Eurozone composite PMI rise to its highest level in June since June 2006. This index measures the activity level of purchasing managers in the services sector.

UK

UK Equities generally performed well over Q2 resulting in some fund managers reporting being overweight in the UK for the first time since 2014. However, the markets did struggle in June due to an increase on Covid infections and concerns around the Delta variant resulting in Boris delaying freedom day. Retail, travel & leisure sectors underperformed in Q2 as one would expect.

Generally, the UK economic outlook showed positive signs as Gross Domestic Products (GDP) forecasts were upgraded and the Bank of England slowed down quantitative easing.

Emerging Markets

Emerging markets saw a strong return in Q2 despite the concerns around US inflation rates being higher than expected and concerns around global monetary policy tightening. Brazil was the best performing market due to the currency strength.

Hungary, Poland & Czech Republic all outperforming due to their economic recovery picking up pace. Russia and Saudi Arabia benefitted from higher crude oil prices. India also performed well despite the surge on covid infections. Peru and Chile were the under performers due to political unrest.

Global Bonds

US treasury bonds declined over Q2 resulting in annualised inflation rates rising to levels not seen in the past 10 years.

European government bonds performed well, amid growing optimism around the region’s recovery and accelerating vaccination programme. UK yields fell slightly following a sharp rise in Q1 and Corporate bonds performed well, outpacing government bonds.

Summary

The risk of interest rates increasing means we will be reducing exposure to Fixed Interest investments in favour of cash.

As global economies continue to recover we do not need to be so defensive with the fund choice and we will be in touch later this month regarding fund changes to be made within the Portfolios.

The information provided in this report is based on our own opinion and offers no guarantee that expectations will be met. Past performance is no guide to future results. As always, should you have any concerns you wish to raise, please do contact us.

Our office is now open and a new phone system should make it easier to contact us even if we are out of the office. Ali is normally in the office every morning, but Ian and Oliver might be out seeing clients.

Keep safe