Despite a New Year rally, which was not sustained, the Markets ended January slightly higher.

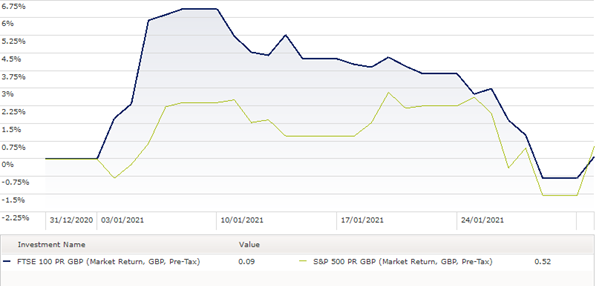

The following chart shows the US and UK market during December. The FTSE 100 represents the 100 largest companies in the UK and the S&P 500 represents the 500 largest in the US. The Dow Jones is often quoted but this only shows the top 30 companies and is dominated by technology companies.

As explained in our recent communication regarding the ongoing format of monthly newsletters, this month there is an overview of the Markets that affect us the most, together with a separate report regarding the investments you hold, detailing the quarterly changes we are recommending.

Market Summary 4th Quarter 2020

The final quarter of 2020 had several twists and turns which resulted in economic and market uncertainty similar to the rest of 2020. That said, quarter four saw equity markets rise following a weak quarter three. Over the year global stock returns were stronger than European and UK returns, with the largest impact coming from the US, Japan and Emerging Markets.

Unsurprisingly, markets reacted to the US presidential election, global pandemic, and BREXIT. However, as we enter 2021 there has been some positive movements in all the above.

The US have signed off their £900bn Covid-19 aid bill, vaccines are being rolled out and the recent Brexit deal provides a positive outlook for the UK economy and the pound.

So, although 2020 in general was very tumultuous and volatile the outlook for 2021 is that of a positive nature with many investors looking towards the end of 2021.

UK

The vaccination programme has provided some positive news for the UK as it is crucial to be able to move forward and reopen leisure and retail sectors. The Office of National Statistics has indicated that household savings have more than doubled from the long-term trend of 8% to over 16%. This could potentially benefit the leisure and retail sectors later in the year as and when social distancing rules are relaxed, and we see our favourite restaurants and shops re open because it means that the average household will have additional money to spend and lost time to make up for which should see in increase in consumer spending. This is expected to impact inflation in the later part of 2021 however in general the outlook for the UK economy remains positive.

US

Despite Covid-19 still raging in the US, the vaccine announcement and the £900bn COVID-19 aid bill have impacted positively on the US stock market.

Within the US there is a theme of the strong getting stronger with Amazon, Nike and Starbucks to name a few have boasted resilient profits in 2020. This is expected to remain the case throughout 2021 as consumer spending habits are focussed on online services and shopping. It will also be of no surprise that the pharmaceutical sector will also be able to ride out the market fluctuations.

The main change for the US will be in the coming months as the Biden administration start to replace Trump’s. Currently it would appear the US have a more balanced leader at the helm and with Biden looking to reset some of the stranger polices from the Trump era such as re-joining the World Health Organisation the outlook for US markets remains positive.

In summary it would seem that 2021 will be dominated by the global pandemic once again however, with the roll out of vaccines, for which the UK are one of the world leaders in implementing this we should start to see some return to normality over the coming months.

There will undoubtedly be some permanent structural changes to economies such as the cultural shift from working in offices to working from home which will have an impact on the cost for office space and ultimately commercial property indices will see the impact of this change. It is also worth being mindful that there will undoubtedly be increases to unemployment throughout 2021 as some companies will sadly not be able to ride out the financial impact of lock downs. This will cause some increase in anxiety for financial markets however, this is not expected to be long lasting.

The information provided in this report is based on our own opinion and offers no guarantee that expectations will be met. Past performance is no guide to future results. As always, should you have any concerns you wish to raise, please do contact us.

Due to the current Covid situation we have closed the office but are still working full time. We are available via telephone and video so please do contact us on 0791 665 2034 for Ian and 0796 459 4210 for Oliver.

Keep safe