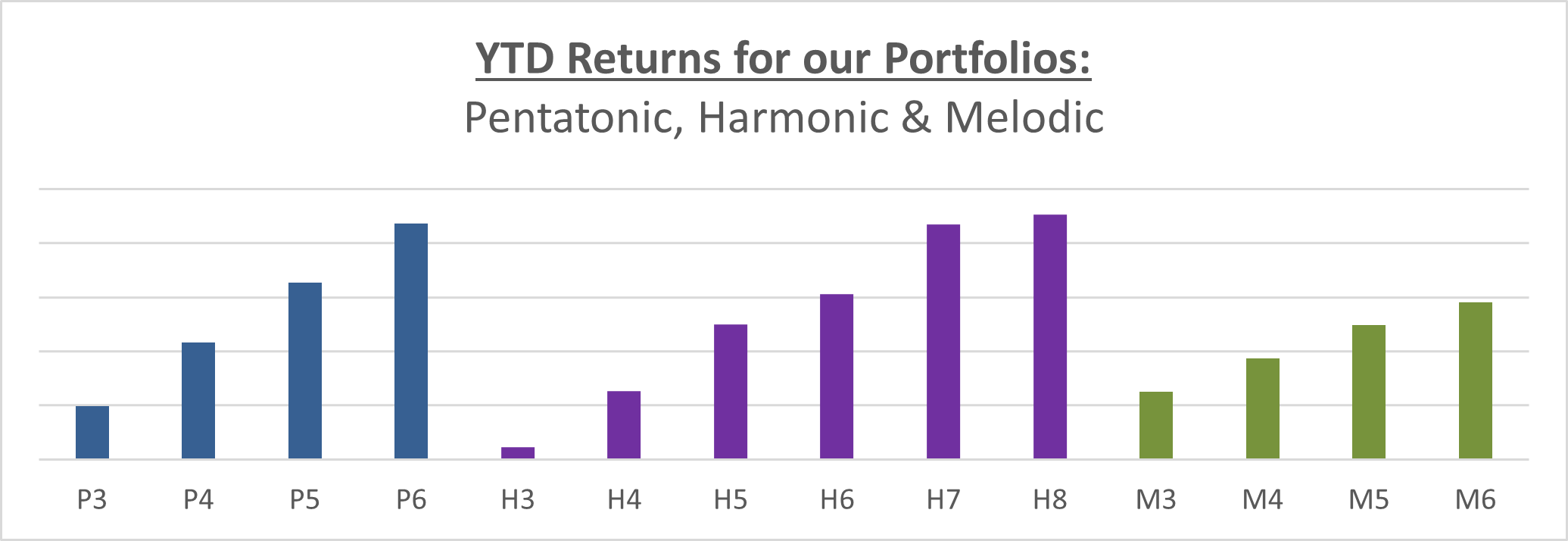

Model Portfolios have all shown a positive return since January 1st as the following table shows. The returns per portfolio are an indication only and are to identify the growth per level of risk within each portfolio range.

The Pentatonic (Income) Portfolios have shown additional growth this year primarily because they lagged the recovery last year. It also calculates total return on the basis dividends are reinvested.

The Melodic range (Sustainable and Responsible Investments) have done better because they have less exposure to Global Fixed Interest funds.

I have reduced the portfolio return by the maximum ongoing fee a client could pay (except Offshore Bond investors). The figures for the Pentatonic Income Portfolio assume income is reinvested as I am unable to strip out the dividend that has been paid.

You may notice I am not showing the growth of the UK and US Stock Markets primarily because the amount exposed to these areas differs according to the level of risk a portfolio is targeting

Market summary 1st Quarter 2021

The end of 2020 saw a significant recovery in markets, with rising optimism on economic growth as vaccines were being rolled out, and confidence that the new year would bring back some normality.

This confidence quickly retreated as we fell back into more lockdowns across the globe as case rates and death rates increased, particularly in the UK where infection rates spiralled much higher. Another lockdown increased pessimism about the economy, although this was offset by the longer-term faith in the vaccine roll-out.

By the end of the quarter an unexpected transformation had taken place as global growth expectations significantly improved, certainly in the UK and the US, as well as in Asia and China. This was led by the effectiveness of the vaccine rollouts in these countries and by the supporting fiscal packages (Government financial support) and monetary easing (keeping interest rates and deposit ratios low in order to make it easier for businesses to borrow money) .

At the same time this transformation led markets to challenge the low growth/low inflation mantra that we have been observing for some time.

The first quarter saw volatility in bond markets as they challenged the levels of yields that had been stable for much of 2020 pushing close to the previous highs of 2018. Whilst inflation has been kept on the back burner for much of the last three years it has now moved to front and centre in the economic debate. This has resulted in Bond Funds showing losses for the year to date. This is considered a low-risk asset but when we see UK Government Bond index trackers fall by 7% since January 1st it identifies that all assets have risk – and also why having exposure to different assets with a broad geographic spread is important.

Equity Markets

The equity markets have made a positive start to the year with most indices delivering positive returns, but the journey has been relatively bumpy with sentiment once again creating frequent periods of uncertainty.

Japan has been the exception to this in that it has fallen since January, albeit it does not represent more than 1% per level of growth – i.e. risk level 6 has 6% exposed to Japan.

Bonds

The narrative has moved from the possibility of negative interest rates in the UK to when policymakers will need to raise rates if rapid growth stimulates inflation. The Bank of England believes the rise in gilt yields – and therefore the reduction in capital value – is consistent with the change in economic outlook. Fixed interest markets therefore face a testing time with higher levels of volatility expected in 2021.

Summary

There have been several market phases since the start of 2020. The first was when growth was disrupted by Covid-19. The second was when significant monetary easing and fiscal support allowed markets to rally. At this stage markets priced in a ‘lower forever’ interest rate regime, but investors are now seeing a shift to a lower but not forever mentality on interest rates.

Whilst politicians want to see growth come back, it can be a dangerous period for financial assets. Today in the States, the Biden administration wants to set a different pathway emphasising wage growth and the administration is likely to pursue this policy despite a risk of higher inflation. Although there has been significant discussion in the financial press about the threat of inflation, the data so far has not really supported the likelihood of any meaningful increase in inflation around the globe. The structural influences of high unemployment and limited wage demands, as well as technological advances, continue to dominate. But this can change, and the bond markets keep testing global financial stability hence the yo-yo nature of markets in the first quarter.

Most investment portfolios have been constructed in the belief that interest rates and inflation will stay low indefinitely and the Covid-19 pandemic has further reinforced the lower for longer interest rate mentality so if anything did rock this consensus there would likely be a nasty market correction.

Looking a little further ahead to the second half of the year, assuming success with the roll-out of vaccines, there could be a sharper than expected upturn in global economic activity.

The information provided in this report is based on our own opinion and offers no guarantee that expectations will be met. Past performance is no guide to future results. As always, should you have any concerns you wish to raise, please do contact us.

Our office is now open and a new phone system should make it easier to contact us even if we are out of the office. Ali is normally in the office every morning, but Ian and Oliver might be out seeing clients.

Keep safe