Most of us are saving in a workplace pension now and with more choices available, individuals have been given more responsibility over their retirement savings.

Research* showed that 77% of savers don’t know how much they’ll need in retirement.

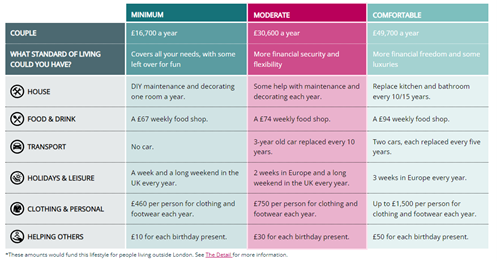

The Retirement Living Standards, based on independent research by Loughborough University, have been developed to show what life in retirement looks like at three different levels, and what a range of common goods and services would cost for each level.

Roughly speaking, a single person living outside of London, that are mortgage or rent free, will need about £11,000 a year to achieve the minimum living standard, £21,000 a year for moderate living standard, and £34,000 a year for comfortable living standard. For couples, it’s £17,000, £31,000, and £50,000 respectively.

The full state pension for 2021-22 is £9,339 per year, which goes a long way to reaching the minimum retirement living standard but this only covers your essential needs, with a small amount left over for fun and social occasions, such as eating out once a month. It does not account for a car or larger household maintenance costs so this isn’t a lifestyle many would aim for.

The moderate lifestyle provides more flexibility, such as a foreign holiday once a year and one car per household and the comfortable lifestyle allows for luxuries such as a nicer car and more trips away.

(Click image to enlarge. Taken from Retirement Living Standards)

As Independent Financial Advisors we can help you by:

- Establishing exactly what your existing pensions will provide and the options they offer

- Find out if you’re entitled to the full state pension

- Discuss the lifestyle you require for later life and whether your pensions will be able to provide this

- Find out the risk levels of your pensions and check they are appropriate – it could be too low as well as too high as a number of ‘default’ funds will be moving your investments to cash and this might not now be relevant.

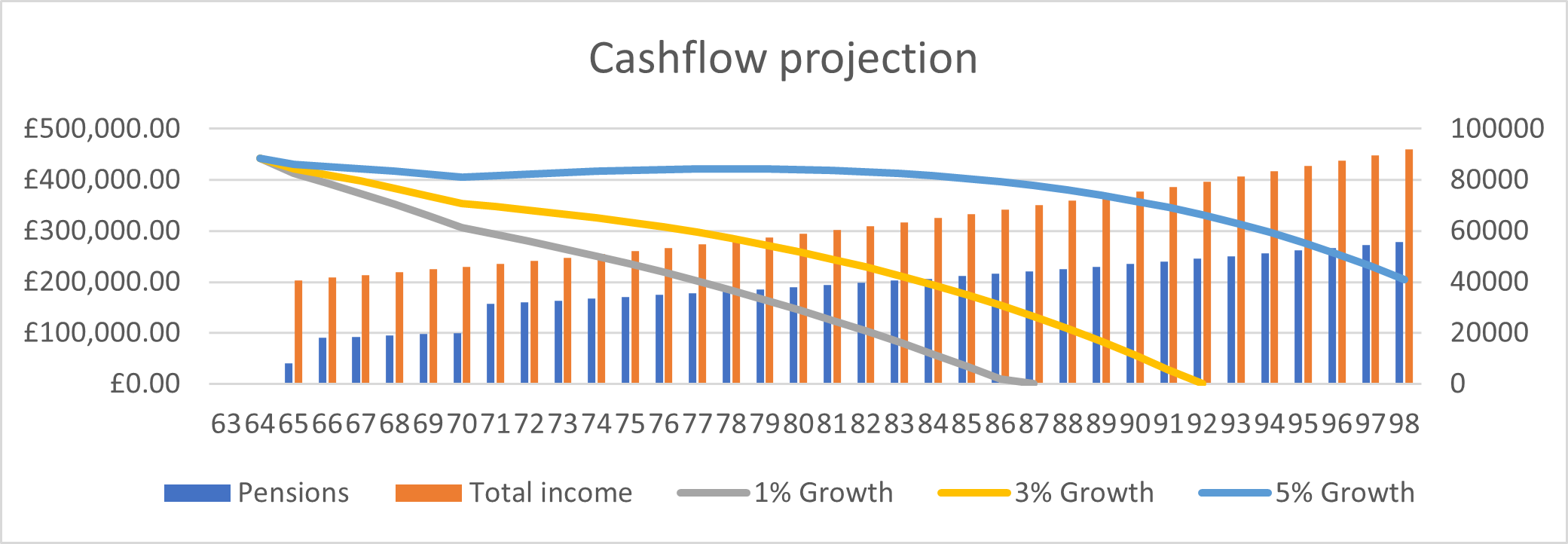

Where required, our clients benefit from a cash flow projection which takes into account savings/pension starting level, ongoing income, state pension payments, inflation and expected growth. This clearly shows the age capital would run out in various situations.

(Click chart to enlarge)

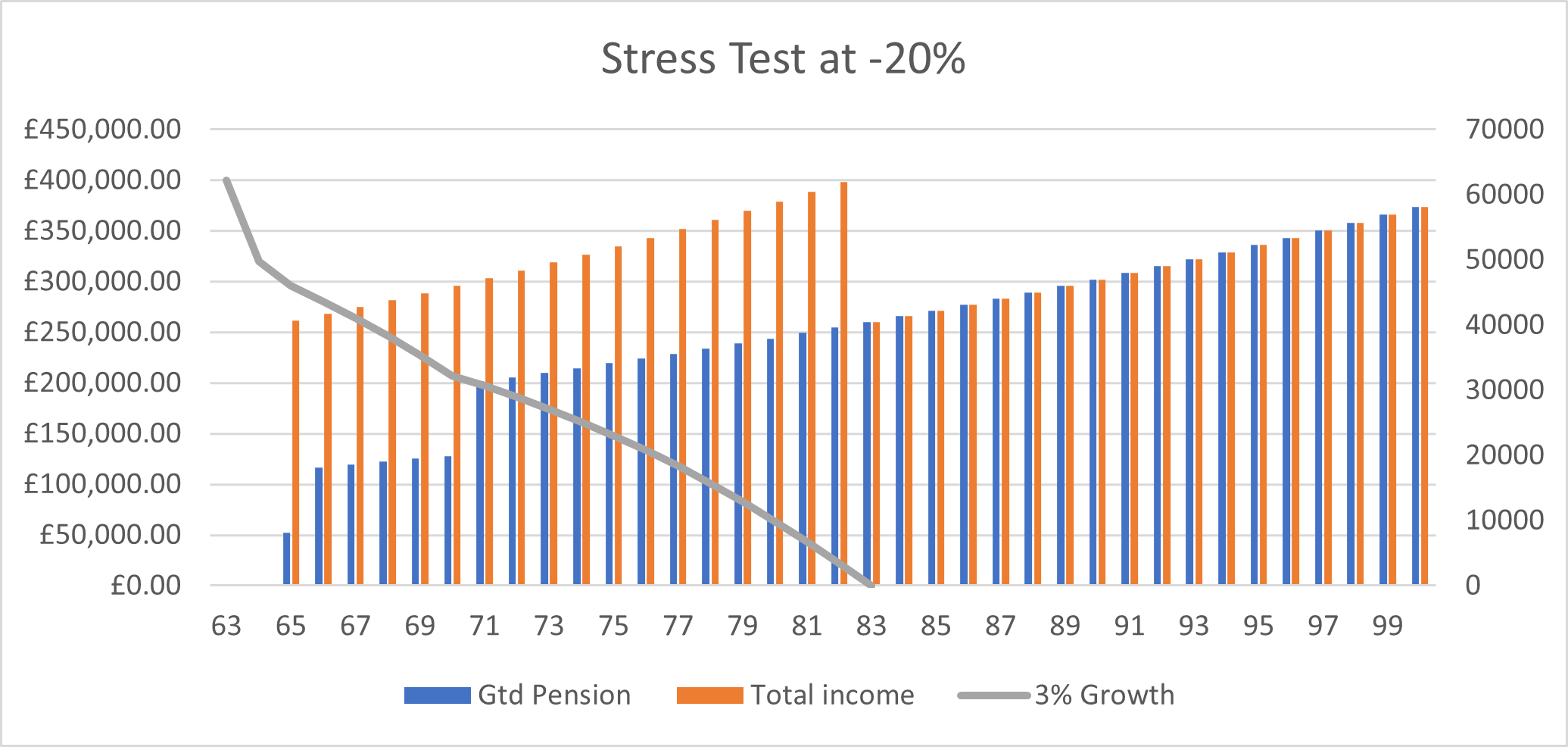

We are also aware that markets do fall as well as rise so we produce a stress test, which shows what would happen if capital fell by 20% and did not recover this loss.

(Click chart to enlarge)

Our service and expertise in financial planning gives our clients knowledge to understand their pension and retirement situation, plus ways to improve their position.

If you are interested in how our services can help you, please contact us for a free initial consultation on:

01803 873978

oliver@personalassetmanagement.co.uk

or use the enquiry form below and we will contact you.

* Independent research by Loughborough University – ‘Retirement Living Standards’ – Home – PLSA – Retirement Living Standards

The value of investments may fall as well as rise. You may get back less than you originally invested.

Pensions are a long-term investment. You may get back less than you put in. Pensions can be and are subject to tax and regulatory change; therefore, the tax treatment of pension benefits can and may change in the future.