With the Markets dropping mainly due to concerns over a potential recession in the UK and USA, this month I want to focus on how this has affected Markets in the past. Whilst inflation is at similar levels to previous recessions, the other financial factors are very different – we currently have low unemployment and low interest rates – and this will have an influence on the way Markets react.

Global Recession?

Interest Rates

With Global levels of inflation, for Developed Markets, being at levels not seen for decades, there is some speculation that we are due for a recession. I therefore wanted to give some information this month on why the Markets are being so volatile and why we have seen a further fall in portfolio values – and why a longer term view is so important.

Unusually, the current levels of inflation are more to do with supply and demand having been affected by Covid than consumer spending. Of course, we have also seen a big increase in fuel costs and this gets passed down the supply chain, with an increase in costs for end users.

The rates of inflation being quoted – expected to peak at 11% in October – relate the previous 12 months and is not a prediction of what will happen in the next 12 months. In fact, the Bank of England is expecting inflation to be down to 3% or 4% over the next 12 months.

In order to help combat inflation Bank Base rates have risen and the Market is expecting – and has therefore priced in – increases of a further 1.5% to 2.5% over the next 12 months within the UK, Europe and USA.

The Global Economic expectation of growth has been revised down but it is still in positive territory and there are few signs yet, that we are about to enter a recession, which is when we have two consecutive quarters of contraction, i.e. negative growth.

Long term investing

As you know, investing is a long-term commitment and we have seen a number of occasions when the Markets have dropped by large amounts. The next section gives some facts and figures regarding a few of the most recent recessions although I have ignored the Covid recession as this was due to exceptional circumstances and the Markets recovered within the year.

I do appreciate when looking at account balances it is disappointing to see capital values having dropped. However, you would only realise the losses if you actually needed to withdraw the capital now. We know Markets recover, we just do not know how long it will take.

If Russia meets a point of being satisfied with the land it has invaded, this will have an immediate positive effect on the Markets. If we see energy prices capped and inflation start to drop, again these are potential positive actions for the Markets.

Please remember that if you are taking regular withdrawals from your capital – rather than dividend income – it is only the capital you are withdrawing that suffers the current level of loss. The remaining capital is still invested and invariably, this is for a long period, during which it will be subject to the movement in Markets.

Previous recessions

Markets do not like uncertainty and when there is talk of a potential recession it becomes nervous and we see movements of 1% or more in a day. However, as with most things in life, when dealing with the facts, a more rational approach can be taken.

This can be demonstrated by the following periods of recessionary concerns when the Markets fell prior the economy actually being in decline.

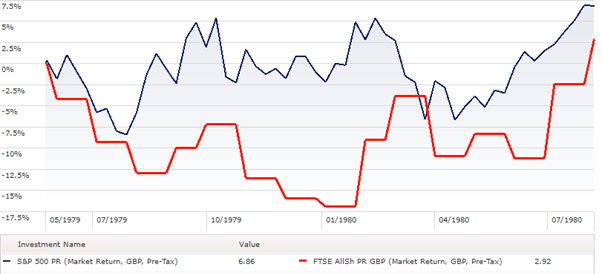

1980 Recession

This was a period of spending cuts and pursuance of monetarism to reduce inflation. It saw a switch from a manufacturing economy to a services economy.

Company earnings declined 35%. Unemployment rises from 5.3% of the working population in August 1979 to 11.9% in 1984. Took thirteen quarters for GDP to recover to its pre-recession peak at the end of 1979. Annual inflation was 18.0% in 1980, 11.9% in 1981, 8.6% in 1982 and 4.6% in 1983. Interest rates generally declined during the recession from a peak of 17.0% at the beginning of 1980 to a low of 9.6% in October 1982.

However, we did not enter a recession until the first quarter of 1980 and we remained in a recession until mid-1981.

1980 Q1: −1.7%

1980 Q2: −2.0%

1980 Q3: −0.2%

1980 Q4: −1.0%

1981 Q1: −0.3%

The chart shows the FTSE All Share Index – as the FTSE 100 did not start until 1984 and the only other commonly used FTSE Index only covered 30 companies! I have also shown the USA S&P as this is unusual in that it is considered a very short recession to have occurred in 1980, followed by a short period of growth and then a deep recession. Unemployment remained relatively elevated in between recessions. The recession began as the Federal Reserve, raised interest rates dramatically to fight the inflation of the 1970s. The early 1980s are sometimes referred to as a “double-dip” or “W-shaped” recession.

You will see that the period of high inflation in 1979 caused the volatility in the Market, and that when we were classed as being in a recession, the Market only took until August 1980 to be back to its May 1979 levels. The UK Market fell by approximately 17% during this period.

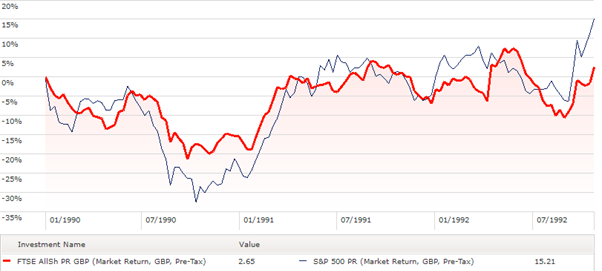

1990 Recession

US savings and loan crisis, high bank rate in response to rising inflation caused by the Lawson Boom and to maintain British membership of the Exchange Rate Mechanism.

Company earnings decline 25%. Peak budget deficit c. 8% of GDP. Unemployment rises from 6.9% of the working population in 1990 to 10.7% in 1993. Took eleven quarters for GDP to recover to its pre-recession peak in the Spring of 1990. Annual inflation was 9.5% in 1990, 5.9% in 1991, 3.7% in 1992. and 1.6% in 1993. Interest rates were stubbornly high initially but declined from a high of 14.8% at the start of the recession to a low of 5.9% by the end of the recession, though interest rates were hiked twice during Black Wednesday.

1990 Q3: −1.1%

1990 Q4: −0.4%

1991 Q1: −0.3%

1991 Q2: −0.2%

1991 Q3: −0.3%

Again, we see that the build up to a recessionary period was more volatile and we saw the UK drop by 20% between January and October 1990. It recovered this drop by March 1991 but remained volatile until October 1992.

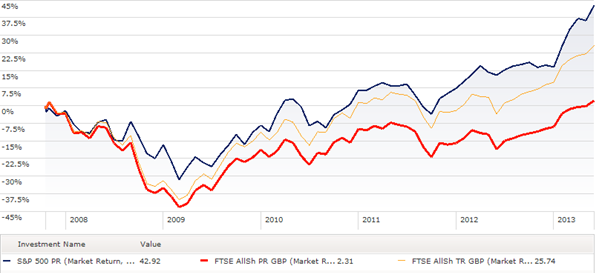

2008 Recession

This was the Credit Crunch with rising global commodity prices and subprime mortgage crisis infiltrating the British banking sector.

The recession lasted for five quarters and was the deepest UK recession since the Second World War. Manufacturing output declined 7% by end 2008. It affected many sectors including banks and investment firms, with many well-known and established businesses having to fold. The unemployment rate rose to 8.3% (2.68m people) in August 2011, the highest level since 1994. There was much speculation of a ‘double dip’ recession during the 2010s, but this proved not to be the case. However, the 2010s saw four separate periods of quarter-on-quarter fall in growth: 2010 Q4 (−0.4); 2011 Q4 (−0.1); 2012 Q2 (−0.5); and 2012 Q4 (−0.2).

2008 Q2: −0.2%

2008 Q3: −1.7%

2008 Q4: −2.2%

2009 Q1: −1.8%

2009 Q2: −0.3%

This subprime mortgage crisis led to the collapse of the United States housing bubble. Falling housing-related assets contributed to a global financial crisis, even as oil and food prices soared. The crisis led to the failure or collapse of many of the United States’ largest financial institutions: Bear Stearns, Fannie Mae, Freddie Mac, Lehman Brothers, and AIG, as well as a crisis in the automobile industry. The government responded with an unprecedented $700 billion bank bailout and $787 billion fiscal stimulus package.

This crisis was out of the blue and started on October 19 2007. The UK kept falling until October 2009 by which time it had dropped 44%. It took until June 2013 to reach its previous level although if you took dividends in to account it was nearly a year earlier.

The chart above shows that despite the crisis affecting the USA, their Markets recovered a lot quicker and this is one reason we advocate diversification within portfolios as exposure to different geographic areas is important.

Summary

It is fair to say that a recession is part of an economic cycle. We see an expansion phase reach a peak, followed by a contraction (recession) which then reaches a trough followed by an expansion phase and so on.

It is not something to be feared as we have had plenty of them in the past and provided you are taking a long-term view on your investment portfolio, I am sure the current market conditions will improve.

The information provided in this report is based on our own opinion and offers no guarantee that our expectations will be met. Past performance is no guide to future results. As always, should you have any concerns you wish to raise, please do contact us.

Best wishes

Ian Pennicott AFPS

Chartered Financial Planner